“Most people don’t understand how to read financial aid award letters,” says Jamie Dickenson, owner of an educational planning service in Charleston, West Virginia, and author of Too Smart for the Ivy League.

That’s true—and perfectly understandable considering that award letters can be confusing because schools use different templates.

Here, experts break down a sample award letter to help you make sense of the information you’ve been sent. While this sample award letter was crafted to be as true to actual award letters as possible, your award letter will likely look different as there’s no standard format schools have to follow. But, the tips here can be applied to all award letters.

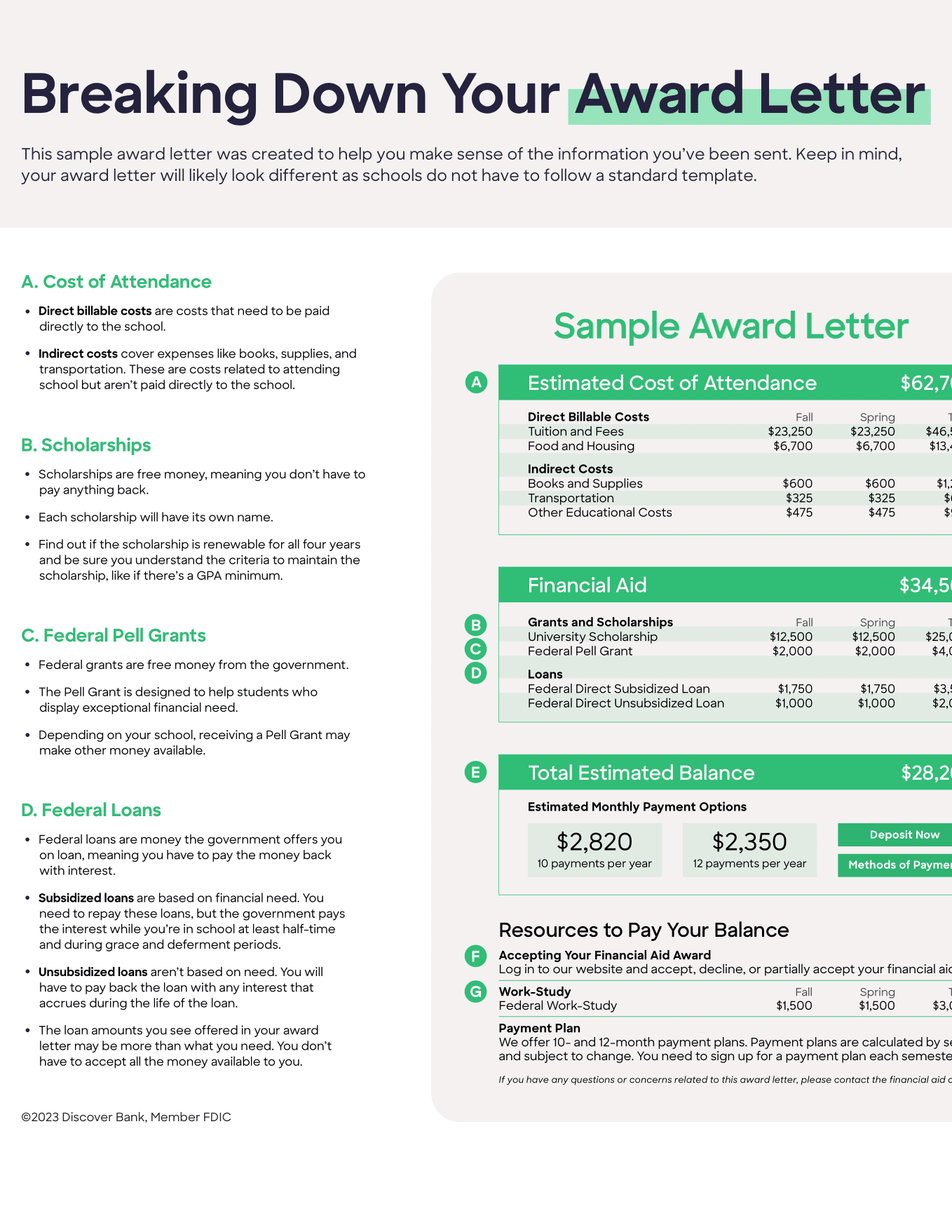

A. Estimated Cost of Attendance

This is the total amount the school estimates that a year of attending will cost, without any aid or loans. Direct billable costs are what they sound like—costs that need to be paid directly to the school. Indirect costs cover expenses like books, supplies, and transportation. These are costs related to attending school but aren’t paid directly to the school. The school is roughly estimating what your indirect costs will be. Since you have a better sense of your spending and needs, you can work up your own budget, which will likely be more accurate than the school’s estimate.

B. Scholarships

A scholarship is free money, meaning you don’t have to pay it back. Scholarships offered by schools all have their own names, but no matter what your scholarship is called, receiving one is good news. Still, Julie Gross, vice president at College Financial Consultants, offers these words of caution for students: “Make sure whether the scholarship is renewable for four years or just a scholarship for freshman year.” If it’s only a one-year scholarship, students should start considering how—and if—they’ll be able to pay for the remaining years of college without the scholarship funds available. She continues, “Some scholarships have a GPA requirement, so it’s something you’d want to be aware of.” Scholarships, like the download shows, can cover a chunk of tuition, so make sure you know what’s required to continue receiving the money each semester.

C. Federal Pell Grants

The Pell Grant is a federal grant designed to help students who “display exceptional financial need.” The maximum amount that can be awarded for 2023-24 is $7,395. Like scholarships, grants are free money—meaning award recipients are not obligated to repay the government. Depending on your school, receiving a Pell Grant may make other money available, says Gross. While this additional money should be listed on your award letter, it’s a good idea to contact the financial aid office to see if anything additional is available to you.

D. Federal Loans

The loans included in your award letter are federal student loans, which are provided by the government. There are three types of federal loans: subsidized, unsubsidized, and PLUS loans.

Subsidized loans are based on financial need. These are loans you need to pay back, but the government pays the interest while you’re in school at least half-time and during grace and deferment periods. Unsubsidized loans and PLUS loans aren’t based on need so you will have to pay back any interest that accrues during the life of the loan. However, making in-school payments can help offset the accruing interest.

If the loan amounts offered in your award letter are more than you need, you don’t have to accept all of it. Gross recommends accepting the free money in your award letter and then considering the subsidized loans before the unsubsidized and PLUS loans because of the interest subsidy. Don’t be fooled by your award letter’s wording, says Dickenson. “The $5,500 offered in loans should really go into costs—you have to pay it back,” she points out. This award letter lumps the loans in with the free grant and scholarship money, but that can be misleading since you have to pay all loans back.

E. Total Estimated Balance

This is the school’s estimate of what you’ll pay for the current school year. This number can be misleading as it only factors in the information from this award letter. It doesn’t account for other loans you may take out, scholarships you could earn, or any money you or your family have saved. It also could miss parts of your indirect costs.

Most schools will offer you some type of tuition payment plan. If you’re interested, you will want to contact the school to find out if there are any fees or interest charges associated with the payment plans offered, says Dickenson.

F. Accepting Your Financial Aid Award

“The offered funds (scholarships, grants, loans, and work-study) are just that: offered,” says Ben Kohl, former president of the Kansas Association of Student Financial Aid Administrators. “A student must follow the instructions provided on the award letter to actually accept the funds.” You can accept the scholarships and grants, even if you don’t accept the loans. “Students think that if they accept their scholarships it commits them to going there,” says Dickenson. That’s actually not the case. If you think this is a school you’re going to say yes to, go ahead and accept the scholarships. You’re not obligated to attend until you actually accept the funds. Note, you do not have to accept all of the loans made available through your award letter. Only accept what you need.

G. Work-Study

Work-study is a federal program that allows you to earn money while in college. But this money is not directly applied to tuition. You’ll receive it in the form of a paycheck like any other job. “A lot of times, schools will put work-study in with the other financial aid, so students think another $2,500 is going to come off the bill,” says Gross. “That’s not the case.”

Work-study jobs are not guaranteed to every eligible student. Students must find, apply, and be hired for these positions. If you do secure a work-study job, the amount of aid listed in your award letter is also not guaranteed. That number represents the maximum amount you’ll be able to receive through work-study. On average, students need to work between 8–10 hours per week to earn the maximum benefit. Of course, that number varies based on the job’s hourly rate, which is often minimum wage for these positions.

Appealing Your Offer

You have the option to appeal your financial aid award letter if your family’s financial situation has changed since filling out the FAFSA® (Free Application for Federal Student Aid). “Contact a representative or officer of the financial aid office to inquire about the appeal process,” says Kohl. If you feel like you deserve more financial aid because your need exceeds your award offer, double-check your FAFSA to see if there’s anything wrong, says Paula Bishop, a college financial adviser in Seattle. In her experience, there’s often something on the tax return that affected the FAFSA that just needs to be fixed to adjust the aid offered.

While your award letter won’t follow this example exactly, it’s important to understand what is included. If anything is unclear, call your financial aid office.

FAFSA® is a registered trademark of the US Department of Education and is not affiliated with Discover® Student Loans.